If you need help, learn more about our Solar Panel Financing Fraud.

$170,000+ recovery

Against Sunlight Financial · Solar fraud arbitration

- $113,000 loan cancelled

- UCC lien removed

- Credit repaired

- $58,000 cash to client

Past results do not guarantee a similar outcome. Every case is different.

Mr. Sanchez thought the knock at his door was just another sales pitch.

By the end of two years, that knock had cost him nearly $240,000, most of it tied to loans and contracts he never knowingly agreed to.

At 75, retired, and living alone in Dallas on his $1,720 Social Security check, he had worked decades to pay off his modest home. It was his pride, his security - until a series of pushy solar panel salespeople promised him big savings, no electric bills, and even a $30,000 “government payment.”

None of it was true.

Instead of savings, the bills piled up: payments to solar lenders he’d never heard of and a utility bill that never went away.

Then came the worst shock - discovering his name and credit had been used to finance solar systems for other people. Installations he had nothing to do with. Loans he had never signed for.

The companies? Vanished.

Phone numbers disconnected.

The paperwork? Full of signatures and e-sign authorizations Mr. Sanchez swears aren’t his.

Now, with multiple lenders at his door and debt he can’t possibly repay, the home he worked his whole life to own is suddenly at risk. In his words:

“So much work to pay off my house… now I can’t sleep thinking they’ll take it away from me. It was all built on lies.”

If any part of Mr. Sanchez’s experience sounds familiar - unexpected debt, forged signatures, loans in your name for someone else’s panels - you may be dealing with identity misuse or outright solar contract fraud. Learn more about high-pressure solar sales tactics.

It breaks our heart to meet people like Mr. Sanchez, and we meet so many like him regularly. At Bennett Legal, we fight against such injustice- to make sure the wrongs are made right, so individuals like Mr. Sanchez can live peacefully, without fearing another debt envelope of dread. Learn more about tax incentive and rebate scams.

In this article, we’ll explain when this crosses the line into illegality and what you can do to fight back before it costs you your home, your credit, or your peace of mind.

“Can They Really Sign My Name Without My Permission?”

Worried homeowner discovers he has more than one solar loan in his name

Worried homeowner discovers he has more than one solar loan in his name

If you’re like most homeowners, the very idea sounds absurd. How could anyone open a loan or contract in your name without you signing something - and have it stick?

The short answer: They can’t. Not legally.

In Texas (where Mr. Sanchez lives) and in most states, signing someone else’s name - or using their personal details to secure financing without authorization - can be both a civil wrong and a crime.

If a solar company, salesperson, or financer uses your identity to sign a contract without your clear consent, it could fall into categories like:

- Forgery (Texas Penal Code § 32.21) - Creating or executing a document that claims to be your act when it’s not.

- Fraudulent Use of Identifying Information (Texas Penal Code § 32.51) - Using someone’s name, Social Security number, or other details to obtain goods, services, or credit.

- Identity Theft (varies by state) - Often prosecuted alongside fraud when financial gain is involved.

- Elder Financial Exploitation (Tex. Hum. Res. Code § 48.002) - Targeting adults 65+ for deceptive, coercive, or fraudulent transactions.

These laws exist for a reason: once a fraudster has your signature (real or fake) on a contract, you’re the one the lender comes after - late notices, collections, and sometimes even liens against your home. That’s exactly the nightmare Mr. Sanchez is living through.

Free consultation

Solar panel contract problems?

We help homeowners fight back against solar fraud. Free consultation.

When It’s Just a Mistake… and When It’s Fraud

Not every unexpected solar loan in your name is a deliberate scam - but in cases like Mr. Sanchez’s, the patterns often point to intentional wrongdoing rather than honest human error.

The difference matters, because while both situations require quick action to protect your credit and stop payments, fraud carries far stronger legal remedies and sometimes criminal consequences for the perpetrators.

Here’s how to start sorting one from the other:

Possible Signs of an Honest Mistake

- The loan agent entered the wrong account or homeowner name in the finance paperwork.

- Your address was mistaken for a neighbor’s or a property with a similar address.

- You were a legitimate co‑borrower but mistakenly listed as the principal borrower.

- Duplicate financing applications due to clerical errors, later corrected.

Clear Signs of Fraud or Identity Misuse(& How to be Prepared)

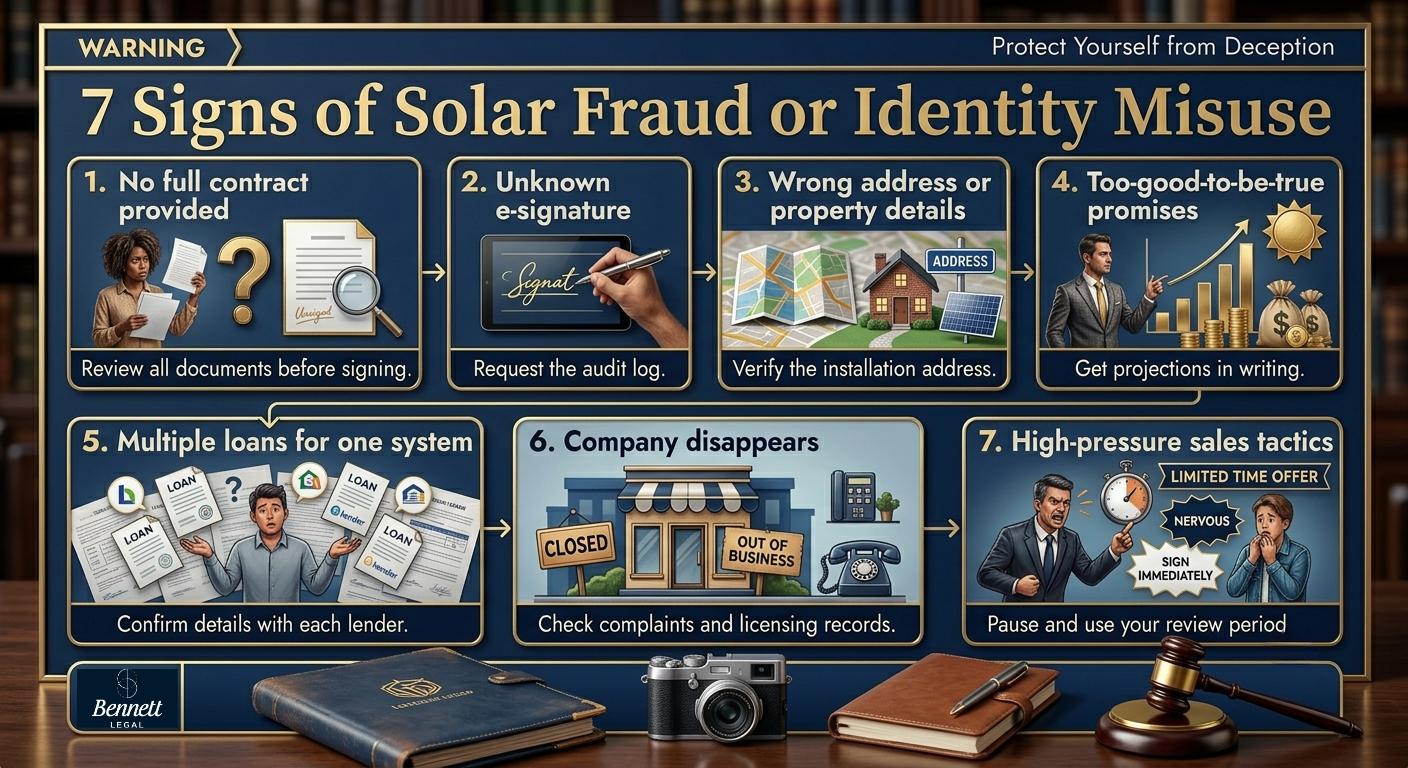

1. Contracts You Haven’t Seen or Fully Read

- Being told, “Don’t worry, we’ll send the paperwork later” or being pushed to sign on a tablet you can’t read clearly is risky.

- Tip: Always get a complete copy - paper or PDF - before you agree, and review it without the salesperson present.

2. E‑Signatures You Don’t Remember Making

- Lenders saying you “signed electronically” when you never opened an email or portal from them.

- Tip: Ask for an audit log showing the device, IP address, and timestamp used to sign.

3. Incorrect Property Information

- The contract lists an address that isn’t yours or includes equipment for another property.

- Tip: Compare every document’s “installation address” to your home address.

4. Promises That Sound Too Perfect

- Sales rep claims you will “never pay another electric bill” or “get thousands from the government” without explaining how.

- Tip: Request all financial projections in writing and verify through independent sources.

5. Multiple Loans or Payment Accounts

- You’re billed by more than one lender for “the same” solar equipment.

- Tip: Call each lender directly to request copies of the signed contract and payment schedule.

6. Difficulty Reaching the Company

- Phone numbers disconnected, emails bouncing, or offices “suddenly closed” after signing.

- Tip: Search for prior consumer complaints online and check state licensing records.

7. Pressure to Sign Quickly

- Salesperson insists the offer “expires today” or discourages you from calling a family member or lawyer.

- Tip: Take at least 72 hours to review - in Texas and many other states, in‑home sales have a legally mandated cooling‑off period.

7 signs of solar fraud or identity misuse

7 signs of solar fraud or identity misuse

Mistake vs. Fraud in Solar Contracts

| Factor | Mistake (Unintentional) | Fraud (Intentional Misconduct) |

| Consent | You signed but in wrong capacity or form | You never signed or your signature was forged |

| Contract Address | Matches your property, slight clerical errors | Belongs to another property entirely |

| Company Response | Acknowledges error promptly, fixes it | Avoids calls, disconnects numbers, denies issue |

| Number of Loans | Single mistaken loan | Multiple loans stacked without resolution |

| E‑Signature Evidence | Matches your own IP/device | Logged from unknown IP/device/location |

| Pattern | Isolated incident | Repeated misrepresentation or concealment |

By holding your situation against this table, most homeowners quickly see which side it falls on.

In Mr. Sanchez’s case, every single marker hit the fraud column - multiple stacked loans, systems installed elsewhere, disappearing companies, and “signatures” he never wrote.

What Happens When Your Identity Is Stolen by a Solar Company? How the Scam Playbook Works

When a solar company (or its salesperson) misuses your personal information, the damage doesn’t stop with a forged contract.

It triggers a sequence of events that can hit your credit, your finances, and even your home security.

Here’s how the playbook often unfolds - and the fallout at each stage.

1. Forged Paper Contracts - You “Agree” Without Knowing It

A rep fills in your personal details - your name, Social Security number, home address - on contracts you’ve never signed, then submits them to a lender as if you approved everything.

Impact on you:

- A legally binding loan in your name without your knowledge.

- Monthly payments start automatically, even if no system is installed.

- Lender collections if you don’t pay - hurting your credit instantly.

2. Abused E‑Signatures - Digital Forgery at Speed

They use your personal data to create a signing account (DocuSign, HelloSign), control it entirely, and “sign” your name without you ever opening the document.

Impact on you:

- Digital records make it appear legitimate unless you challenge them.

- Disputing an e‑signature can require legal proof, slowing down your defense.

- Lender and credit bureaus may initially assume you authorized the account.

3. Cross‑Property Financing - You Pay for Someone Else’s Panels

Your identity is used to finance a solar system at another property, often belonging to someone who wouldn’t qualify for credit alone.

Impact on you:

- You’re liable for thousands in equipment costs for panels you’ll never use.

- Potential lien filed on your property for equipment installed elsewhere.

- If the other party defaults, your credit and property are still at risk.

4. Loan Stacking - Crushing Debt by Design

They convince you to “fix” your system by adding more panels or replacing parts - but instead of paying off your first loan, they simply add a new one.

Impact on you:

- Double or triple payments every month.

- Loan obligations that can last 20–25 years.

- Risk of foreclosure if liens are filed for non‑payment.

5. Fake Payoff or Consolidation Promises

They tell you they’ll merge multiple loans into one “lower payment,” but instead, they open yet another loan without closing the originals.

Impact on you:

- Three or more active accounts in your name at once.

- Severe debt‑to‑income ratio damage, wiping out future borrowing power.

- Aggressive collector calls from multiple companies.

6. Ghost Companies - Vanishing Overnight

Once contracts are locked in, the company disappears - disconnected phones, fake addresses, dead websites.

Impact on you:

- No recourse for faulty or incomplete work.

- You’re left paying for a system that may never work properly.

- Repair and removal costs fall on you, not them.

The Domino Effect - How One Forged Signature Can Spiral

When your name is misused in this way, the harm stacks fast:

- Immediate debt in the tens or hundreds of thousands.

- Credit score plunge from missed or disputed payments.

- Liens or UCC filings that cloud your home title.

- Years of legal disputes to clear your name.

- Severe stress, anxiety, and lost sleep, especially for seniors or fixed‑income homeowners.

Bottom line: This isn’t just a contract issue - it’s a form of identity theft that weaponizes your personal information against you.

The earlier you spot something wrong, the greater your chances of containing the damage.

Immediate Action Steps if You Think Your Name Was Used Illegally

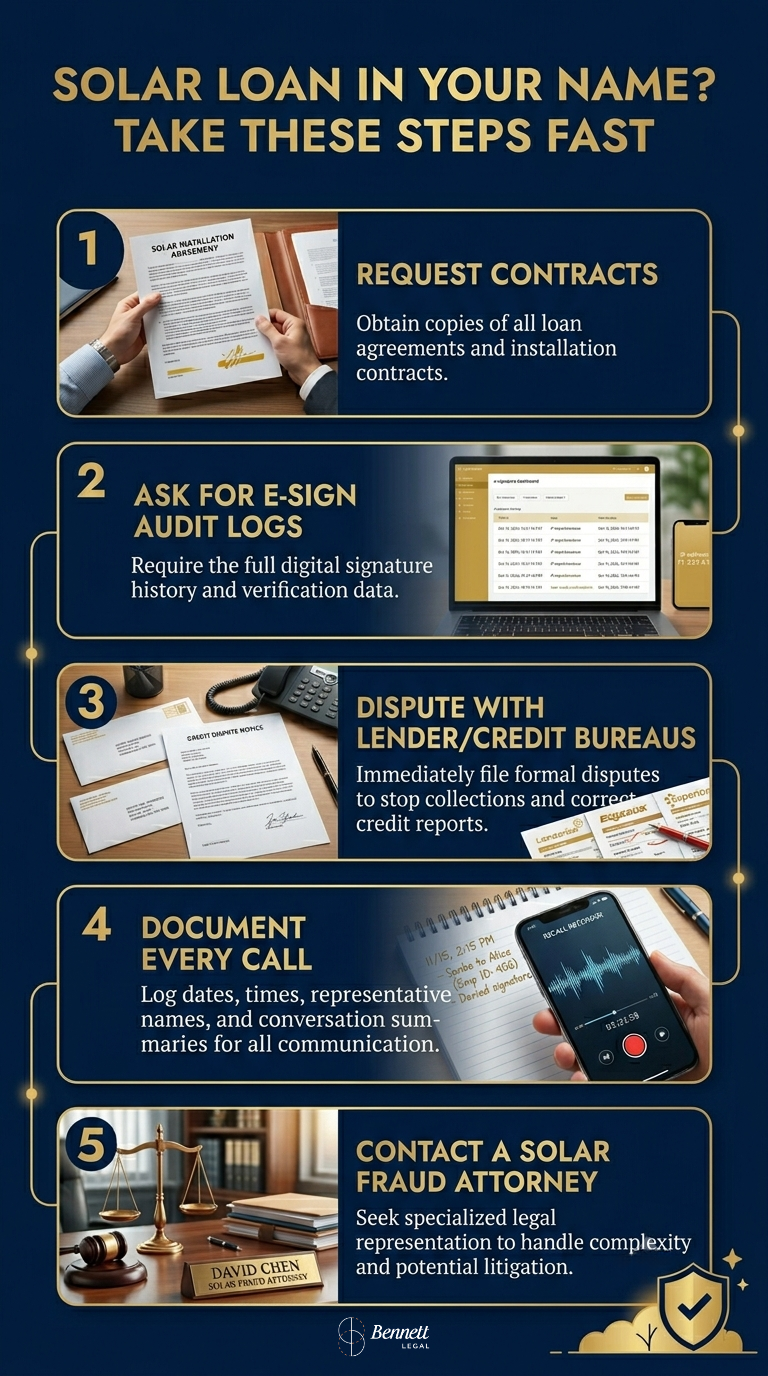

Steps to take if you have a solar loan in your name without consent

Steps to take if you have a solar loan in your name without consent

If there’s even a chance your name or personal details were used to open a solar loan without your consent, every day matters. The faster you act, the more likely you can stop the financial bleed and document the case for legal relief.

Here’s what you should do - starting today:

- Pull Your Credit Reports Immediately

- Go to AnnualCreditReport.com and check all three bureaus (Experian, Equifax, TransUnion) for loans, inquiries, or accounts you don’t recognize.

- Look for any “hard inquiries” from solar finance companies.

- Freeze Your Credit

- A freeze stops new accounts from being opened in your name until you unfreeze it.

- In Texas, credit freezes are free by law, regardless of age.

- Gather All Paperwork & Communications

- Contracts, emails, texts, door hanger cards, business cards, invoices - every scrap could be evidence.

- If the company only gave you electronic access, download and save all PDFs before they lock you out.

- Request E‑Signature Audit Logs from the Lender

- These logs show the IP address, device, and location where the document was signed.

- Send Written Disputes to Each Lender

- Use certified mail with “return receipt requested.” Clearly state you did not authorize the loan.

- File an FTC Identity Theft Report

- Start at IdentityTheft.gov to create an official affidavit.

- Contact the Texas Attorney General’s Consumer Protection Division (or your state AG)

- Many AG offices have active solar fraud investigations.

Call Bennett Legal

Our team has experience battling solar panel identity fraud cases and can move quickly to freeze fraudulent accounts, dispute liens, and launch claims under both federal and state law. We know which agencies act fastest, and we make sure your case gets priority status with lenders.

Legal Rights & Protections If Your Name Was Used Without Consent

Texas Protections:

- Texas Penal Code § 32.21 (Forgery): Classifies forging a document that affects property or credit as a criminal offense.

- Texas Penal Code § 32.51 (Fraudulent Use or Possession of Identifying Information): Felony charges for using another’s name, DOB, SSN to obtain goods/services.

- Texas Deceptive Trade Practices Act (Tex. Bus. & Com. Code § 17.46): Allows triple damages if the victim is 65+.

- Property Code § 50: Improper liens on a homestead can be challenged and removed.

Federal Protections:

- Truth in Lending Act (TILA): Requires clear, informed consumer consent before establishing credit.

- Fair Credit Reporting Act (FCRA): Gives you the right to dispute inaccurate accounts and requires bureaus to investigate within 30 days.

- Identity Theft and Assumption Deterrence Act (18 U.S.C. § 1028): Federal crime to use another’s identity for unlawful purposes.

- Magnuson‑Moss Warranty Act: May apply if the system comes with misrepresented warranties.

Other State Examples:

- California: Penal Code § 470 (Forgery); Civil Code § 1798.93 (civil remedies for identity theft) plus 3‑day Home Solicitation Sales Act rescission.

- Florida: Fla. Stat. § 817.568 (Criminal Use of Personal ID), FDUPTA consumer remedies.

Elder Protections

If you are 65 or older, you may qualify for enhanced legal remedies:

- Texas DTPA § 17.46(b)(27): Automatic eligibility for treble (triple) damages in proven fraud cases.

- In many states, elder financial exploitation carries stiffer penalties and can trigger priority investigation by adult protective services.

- Special restitution funds may be available for seniors targeted by home improvement fraud.

Exceptions & Procedural Barriers

Even strong identity theft claims have hurdles:

- Arbitration Clauses:

- Many solar contracts bury mandatory arbitration in fine print.

- Fraud can sometimes be used to void an arbitration clause, but you’ll need legal help to argue it.

- Statutes of Limitations (SOL):

- In Texas, the SOL for fraud is generally 4 years, but may be tolled (paused) until you discover the fraud.

- For identity theft disputes under the FCRA, you have 2 years from discovery, 5 years max from violation.

- Proof of Non‑Consent:

- You’ll need more than just saying, “I didn’t sign.”

- IP logs, handwriting comparisons, and witness testimony can strengthen your case.

- Lender Pushback:

- Some lenders insist on payment until the fraud is “proven” - which can take months.

- Quick legal intervention is key to avoid collections and credit damage.

- Liens/UCC Filings:

- Even if the loan is fraudulent, removing a lien on your property may require a court order or notarized lender release.

State‑by‑State Cooling‑Off & Identity Theft Law Quick Chart

| State | Cooling‑Off Period for In‑Home Sales | Key Identity Theft Statute | Senior Protections |

| TX | 3 business days (Bus. & Com. Code) | Penal Code § 32.51: Fraudulent Use of ID | Treble damages under DTPA § 17.46 |

| CA | 3 business days (Civil Code § 1689) | Penal Code § 530.5: Criminal ID Theft | Elder Financial Abuse Act: enhanced civil |

| FL | 3 business days (§ 501.025) | Fla. Stat. § 817.568: Criminal Use of Personal ID | Exploitation of Elderly (§ 825.103) |

| NY | 3 business days (Gen. Obligations) | Penal Law § 190.78: ID Theft in the First Degree | Enhanced sentencing guidelines |

| IL | 3 business days (815 ILCS 505/2B) | 720 ILCS 5/16G: Identity Theft | Treble damages in some consumer actions |

Your Name, Their Scam: Stopping Solar Companies from Stealing Your Identity

Digital solar contract showing suspicious e-signature details and audit log information

Digital solar contract showing suspicious e-signature details and audit log information

Having your name, credit, or even your home tied to fraudulent solar contracts isn’t just a paperwork mistake - it’s identity theft dressed up as “green energy.”

What happened to Mr. Sanchez should never happen to any homeowner, yet cases like his are rising across the country. The time this blog is published, we are fighting for Justice for Mr. Sanchez.

When companies forge signatures, misuse personal information, or bury seniors in loans they never agreed to, they cross the line from aggressive sales into outright fraud.

At Bennett Legal, we don’t let that stand. We fight for homeowners whose trust and financial security have been stolen by predatory solar companies.

Our team acts quickly to:

- Freeze fraudulent accounts before the damage grows.

- Remove illegal liens and fight lenders demanding payment on forged contracts.

- Leverage state and federal fraud laws to unwind fake agreements and pursue damages.

- Protect vulnerable seniors who are entitled to enhanced remedies under consumer protection statutes.

You worked hard for your home, your credit, and your peace of mind. Don’t let a forged signature or stolen identity strip that away.

📞 Call Bennett Legal today. We’ll review your case, explain your rights, and take swift action to stop fraud in its tracks - so you can live without the fear of losing everything to a crime you never consented to.

FAQs

1. Can a solar company open a loan in my name without my permission?

No - under both Texas law and federal consumer protection statutes, opening a loan in your name without your informed consent is illegal. It can constitute forgery, fraudulent use of identifying information, and identity theft. If this happens, you may have both civil (lawsuit) and criminal remedies available.

2. What if my signature on the contract is forged?

A forged signature makes the contract voidable - meaning it can be canceled once proven. You may need evidence such as handwriting analysis, forensic review of e‑signature logs (IP address, device ID), or witnesses who can confirm you never signed.

3. How do I dispute a fraudulent solar loan?

- Contact the lender in writing (certified mail).

- File a dispute with all three major credit bureaus under the Fair Credit Reporting Act (FCRA).

- Submit an FTC Identity Theft Report via IdentityTheft.gov.

- In Texas, also file a police report - this strengthens your case with lenders and credit bureaus.

4. Can I remove a lien placed because of a fraudulent solar contract?

Yes, but the process depends on whether the lender agrees it was fraud:

- Voluntary release: If the lender concedes, they can file a lien release with your county clerk.

- Court order: If they refuse, you may have to bring a quiet title action or similar proceeding.

- This is where a firm like Bennett Legal can step in to expedite the process.

5. How quickly do I have to act once I discover the fraud?

Immediately. The longer you wait:

- Payment defaults can damage your credit.

- Arbitration clauses and statutes of limitation can start running.

- Fraudulent liens can complicate refinancing or home sales.

Acting within days - not weeks - can make a major difference in outcomes.

6. What protections do seniors have in identity theft cases like this?

In Texas, if you are 65 or older, the Deceptive Trade Practices Act allows triple damages for proven fraud. Other states impose enhanced criminal penalties for elder financial exploitation and sometimes provide accelerated court scheduling for senior cases.

7. Can Bennett Legal help if the solar company is out of business or won’t return my calls?

Yes. We can pursue the finance companies, lienholders, and - in some cases - the contractor’s bond or insurance. We have strategies for unresponsive or “ghosted” companies, including working with state agencies and escalating to litigation.

Related Reading

Free consultation

Solar panel contract problems?

We help homeowners fight back against solar fraud. Free consultation.